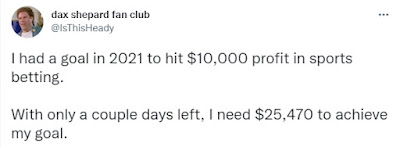

The above Twitter account is clearly not a follower of this blog, but sadly is likely representative of the majority of punters out there. Sports betting isn't the easy road to riches that it is often claimed to be, but for those with discipline and the right analytical skills, it can still be a lucrative hobby.

My daughter gave me "The Retirement Handbook" by Ted Heybridge for Xmas, which included the advice to "learn to love spreadsheets." I think I may be ahead of the game in this category, especially when it comes to the encouragement regarding financial spreadsheets to "check this regularly, perhaps on a set day of the month."

Day? Unless I'm away from home, I check / update it on almost hourly basis! Perhaps a slight exaggeration, but I do tend to monitor things a little closer than is generally considered healthy, a habit that I should perhaps consider for addition to my list of 2022 resolutions, which otherwise looks remarkably similar to my goals for 2021, 2020 and just about every year since becoming an adult - using the legal definition since acting like a grown up seems to continue to elude me.

My three weeks away is now at an end, a trip encompassing events including, but not limited to, the internment of my Mother's ashes in north Devon, several days at my sister's farmhouse in rural Kent, a stay at my son's new home in West Sussex and the rather depressing task of clearing out the family home of 66 years as my Dad now needs full time care and is in a care home. Visits to see him were paused due to staff members testing positive for COVID, and the Disney on Ice spectacular at the O2 was cancelled on the morning of the show although as this was grandad's treat paid for back in August, the refund will come in handy, even if it won't hit the books until next year. A first ever visit to Bluewater was the replacement activity with ice skating an acceptable substitute activity for the granddaughters even if the funfair was ridiculously expensive!

We still have a few more hours of trading before the year end numbers are in, but barring an October 19th, 1987 scenario, December, Q4, H2 and 2021 should all be nicely in profit. The US Markets will also be open on Monday so no New Year Holiday over there due to the rule:

that the exchange will be closed either Friday or the following Monday if the holiday falls on a weekend, unless “unusual business conditions exist, such as the ending of a monthly or yearly accounting period.”

With December 31st obviously the end of a month, quarter and a year, there is no respite for traders there and a weekend to update my numbers is an added bonus. For those following my advice to invest in the S&P 500 over the FTSE, another win for the former makes it five years in a row and 12 "wins" in the last 13 years. I'll have the precise numbers some time over the weekend.

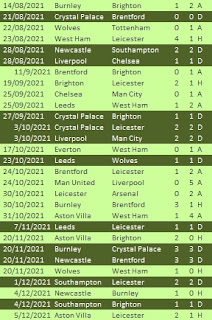

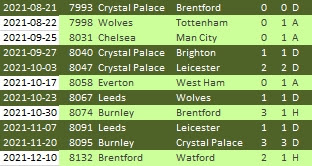

The EPL Draw System was very quiet while I was away, with only one match qualifying as "Close" which was the Brentford v Watford game on December 10th, won 2:1 by the home team thanks to a 96th minute penalty. This match was also a Toss-Up selection, and the ROIs for the 2021-22 season to date are now 79.7% for the Toss-Ups and 35% for the Close selections. Several matches were postponed and the league table currently looks like those from my youth, where a difference of several games in the 'Played' column between clubs was par for the course. Results for the Toss-Up selections at the turn of the year are as shown here:

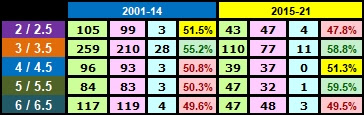

My Crystal Palace have certainly played their part so far, and a notable lack of Big 6 clubs featuring in the selections. Only Nine of the 60 clubs selected in the "Close" category have been Big 6 clubs.

Another reason why there were so few selections is that the average "difference" in December's 52 matches was 65.7%, a much higher number than the 52.3% for the rest of the season, and 34 matches had an odds-on favourite.

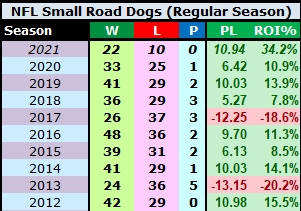

In the NFL, Small Road Dogs are now 40-24, an ROI of 22%, with two more weeks of the regular season remaining.

In the NBA the edge for Unders on Totals of 212.5 or higher seems to have faded somewhat while I was away but still up on the season with a gain of 25.3 points and an ROI of 6.8%. With December looking to be a losing month though, I need to take a look at the data before I resume betting on these.

A Happy New Year to all of you as this blog enters its 15th year with the next post, a summary of 2021 and a look ahead. Stay safe, and take care tonight.