You may have come here,

Seeking the rules,

In which case you’ve fallen,

For Cassini’s April Fool’s

New Milton Advertiser - Saturday 24 January 1976Not a good weekend for Norman LeighLast weekend was not a very good one for Mr. Norman Horace William Leigh (47), of 11, Nelson Place, Lymington.The "Sunday Mirror" published an investigation into his activities, and on Monday he appeared at Lymington Magistrates' Court where he was fined £10 for being drunk and disorderly the day before in the High Street and Captain's Row,The "Sunday Mirror" article dealt with an investigation into Mr. Leigh's past, and his offer to the public suggesting they could earn large sums if they bought his infallible gambling system. His posters read: "Earn up to £475 a week working in London or on the French Riviera (no selling involved). Full details without obligation".For only £100 plus 25 per cent of the winnings, Mr. Leigh will sell the secret of his roulette system. He said his plan was to recruit 100 people to play the roulette tables as individuals at clubs in London and on the French Riviera. "By working inconspicuously at roulette four hours a day, for five days a week, 100 people could gross £50.000 a week of which, by contract, my share would be £12,500." he told Lawrence Turner, who did the investigation.In case anyone might be anxious to try their luck, the "Sunday Mirror" also revealed that Mr. Leigh has a record as a confidence trickster, and was sentenced to five years in jail in 1970 for what the prosecution called "a heartless fraud on people seeking homes." Mr. Leigh claims he was framed.

From the Daily Telegraph's Obituary pages, 5 July 2015:

Ron Pollard, who has died aged 89, changed the face of British betting by taking the bookmaking business beyond horse and greyhound racing into the more exotic arenas of beauty contests, politics, book prizes and the arrival of aliens from outer space.

Guided by his principle that “betting should be fun”, Pollard’s genius was to realise that many punters would cheerfully bet on outcomes far less likely than their being struck by lightning. “It was abundantly clear”, he once said, “that the public would gamble on absolutely anything. If it moved, if it was on TV, if it caused an argument in a pub, they wanted to bet on it.”

His aim was always for his firm, Ladbrokes, to be first with anything new, thus raising its profile and encouraging more punters to use it. Having introduced betting on cricket, golf, tennis, darts and snooker, in 1977 Pollard offered odds on the existence of the Loch Ness Monster; in the same year Ladbrokes started to take bets on the arrival of aliens on Earth, giving 500-1 to a group in California run by a woman who claimed to be a reincarnation of the Mona Lisa.

Pollard offered odds of 1,000-1 against Elvis Presley returning from the dead. Although he conceded that this was a “tasteless exercise”, Ladbrokes took so much business that it soon had a £2·5 million liability, and he had to cut the price to 100-1. The safest bet he ever laid was placed by a teenage girl: 5,000-1 against her taking tea with a reincarnated Elvis by the end of 1982.

Although these stunts were not always profitable – Ladbrokes had offered 100-1 against a man walking on the moon in the 1960s – he appreciated that they reaped for his firm “the most precious commodity of all: publicity”.

Pollard did not attribute his success entirely to his own acumen. He was a self-confessed spiritualist who believed that he was guided by a 15th-century bearded Chinaman in a white skull-cap. His interest in this field had been aroused in 1955 when, aged 29, he accompanied his mother-in-law to Kennards, a department store in Croydon, where she consulted a medium.

Although then a sceptic, Pollard also saw the medium, who caressed the young man’s comb before pronouncing: “Goodness gracious, I wish I was going to have your life. You are going to be in all the papers, everyone wants to know what you are saying, and you are going to Buckingham Palace [to] meet members of the Royal Family.” It was she who alerted him to the presence of his Chinaman. Twenty-four years lat er Pollard was honoured as “Spiritualist of the Year”.

His greatest coup came in 1963, when he introduced betting on politics with the “Tory Leadership Stakes”: “For two weeks I did not know if I was a bookmaker or a film star. The telephone did not stop ringing. I was constantly on television and radio. Everyone wanted a quote.” Sir Alec Douglas-Home (the eventual winner, who had initially ruled himself out of the contest) was installed at 16-1; Ladbrokes took £14,000 on the exercise, making a profit of only £1,400. But the company was now known across the world.

At the next general election, in 1964, Ladbrokes opened a book. The hotelier Maxwell Joseph bet £50,000 on a Labour victory, winning £32,272 when Harold Wilson emerged with a five-seat majority. Had the Tories won, the firm would have lost £1·5 million — money it did not have. Pollard was so concerned about this outcome that he resolved to commit suicide in the event of a Conservative victory.

The £640,000 that Ladbrokes took on that election was the record at the time for any single event (including the Derby or the Grand National). In the general election of 1966 the firm took £1.6 million.

Before long, Pollard was being entertained by MPs at the House of Commons. At the time of the Conservative Party’s leadership election of 1975 he was invited to lunch at White’s, where someone inquired what odds he was offering on Margaret Thatcher to win the Tory leadership. Pollard replied: “Fifty to one.” Pollard’s companion confided: “I would be very careful if I were you.” The odds were immediately slashed to 20-1.

Occasionally, Pollard’s political antennae (or his Chinaman) let him down, as in the general election of 1970, which the Conservatives unexpectedly won, costing Ladbrokes around £80,000. Some members of the board wanted Pollard sacked; but the chairman, Cyril Stein, remained loyal, telling his colleagues: “If he goes, I go.” The odds-maker survived.

Ronald James Joseph Pollard was born in London on June 6 1926. His paternal grandfather distributed relief money to the unemployed, and would visit pubs in Southwark disguised as a chimney sweep to see if any of his clients were spending their welfare on beer. Although Ron’s father was the accountant to a mineral water company, the family had little money and his mother worked from home as a glove machinist. At school in Peckham Ron failed to shine academically but enjoyed playing football and cricket. He left with no qualifications.

He got a job as an office boy in a building firm at Peckham, learning bookkeeping. On Saturdays he went greyhound racing at Catford. Then, in 1943, he became a ledger clerk with William Hill at the bookmaker’s office in Park Lane. At first he ran errands, such as paying a jockey who had obligingly finished second on a hot favourite at Goodwood. At this stage Hill’s was operating illegally by handling cash betting, which was then allowed only on the racecourse (transactions off-course had to be on a credit basis).

Although he was called up for the Army, Private Pollard was still at Westcliff-on-Sea on VE Day. He then served on the Gold Coast, where he was promoted to sergeant and won the Gold Coast ping-pong championship two years in succession.

He returned to Britain in 1947, and was demobbed the following year, returning to work for William Hill. He was made a course clerk, recording the bets taken by the Hill’s representative, and occasionally acting as the bookmaker at some of the smaller meetings; he was then appointed manager of the accounts department.

Pollard joined Ladbrokes as credit manager in 1962, the year the firm opened its first betting shops. “These were still the days of credit betting, and you had an account with Ladbrokes at their Burlington Street offices only if you were in Debrett,” he said. “If you were in trade, no matter how prosperous, you had no chance of an account with the firm that had a direct telephone link to Buckingham Palace for the regular royal bets that would be struck, sometimes daily.”

Before long he had been appointed general manager of Ladbrokes, and, in 1964, he was made a director of Town and Country Betting, the Ladbrokes holding company which was to become Ladbroke Racing. In the same year he became the firm’s PR director, remaining there until his retirement in 1989.

Among Pollard’s most famous stunts were his forays into the Miss World contest. These did not endear him to the organisers, Eric and Julia Morley. After Julia Morley accused him, apparently without irony, of “dragging [the contest] into the cattle market”, and banned him from the Miss World rehearsals in a television studio, Pollard disguised himself as a carpenter (complete with overalls, cloth cap and a tool kit) and spent a morning assessing the attributes of the candidates on whom he was to make a book.

On another occasion he assumed the character of a waiter, sporting a false grey moustache, to penetrate the dining room at the Dorchester where the finalists were attending a function. Pollard was extremely successful in predicting the outcomes of Miss World, and in 1982 personally won £5,000 when Miss Dominican Republic took the title. His guiding principle was: “The sexy ones never win.”

When it came to fixing odds for the Booker Prize, Pollard would read the first 60 or so pages of a novel; a similar number in the middle; and the final 60.

Pollard himself was not a habitual gambler (betting “only when I thought I knew something”) and did not have a high opinion of those who were: “The reason why people bet has nothing to do with money. They do it because they want to get one up on the other fellow and because they want to be right.”

He was an entertaining man and a fine raconteur who courted, and made many friends among, the press. A lifelong socialist, his greatest regret was that he never became an MP; he claimed to have been offered a seat by all three main parties.

In 1991 he published an autobiography, Odds & Sods: my life in the betting business.

Ron Pollard is survived by his wife, Pat, and three children.

Ron Pollard, born June 6 1926, died June 10 2015

It took Navinder Singh Sarao a long time to accept that he might have been scammed out of $50 million. Stuck in London’s Wandsworth prison, wracked with anxiety and unable to sleep, the realization dawned on the man dubbed the “Flash Crash Trader” as slowly as spring turned to summer outside the barred window of his jail cell.

The trauma of the past few weeks had been difficult to process. On April 20, 2015, the slight, doe-eyed 36-year-old had dozed off peacefully in the same suburban bedroom he’d slept in since he was a boy. The next day he was arrested and taken to a police station, where he was charged with 22 counts of fraud and market manipulation carrying a maximum sentence of 380 years.

According to the U.S. government, the British day trader had made tens of millions of dollars using an illegal practice called spoofing, including, fatefully, on the morning of May 6, 2010, when the Dow Jones Industrial Average fell almost 1,000 points in minutes before bouncing back. The extent of Sarao’s culpability for the flash crash is fiercely contested, but the incident exposed the shaky foundations on which the hyper-fast, computer-dominated financial markets now rest.

Sarao’s bail was set at 5.05 million pounds ($6.3 million). It was a hefty sum, but according to the accounts of his company, Nav Sarao Futures Limited, he’d earned 30 million pounds in the previous five years. Newspaper reports, in which Sarao was dubbed “The Hound of Hounslow,” speculated that he’d be back with his family in the shabby West London borough by the weekend.

To clarify what I mean when I say 'official' results, since there is unfortunately no recognised source for closing prices (or starting prices to use the horse racing term) for any sport with which this blog concerns itself.

From Nikolai Livori - Sportsbook Soft or Sharp

The sports betting industry is fragmented into Sharp and Soft books, and of course a mix in between. But what does this mean? We use a more precise term by referring to them as Asian and European books respectively - with Asian books being sharper than European ones.

Soft bookmakers like the renowned Unibet, Betsson, William Hill etc. make use of a lot of traders within the company that use manual or semi-automatic odds movements to ultimately rely on gut feelings, knowledge and game statistics within the industry. They operate with high margins. They do not welcome sports traders and most of the time limit such customer accounts thus falling into the trap called a “false positive”. What if the person you just limited could have been one of your VIP Casino players? Soft bookmakers like these target mostly punters and gamblers and usually have other products to support their sports book such as Casinos, Poker, Bingo etc.

The Sharp bookmaker model is based mostly on mathematical and highly efficient automatic risk management tools. They do employ traders as well to compile odds, however balancing their book is sharper and done with the help of mathematical models. Most of the time they are able to offer better prices in the industry, due to being faster and sharper than Soft bookmakers. Most of them also do not limit bettors and accept large bet stakes, thus they welcome traders and punters alike. Examples of such books are Pinnacle Sports, ED3688, SBOBet etc. Their profit is derived on smaller margins due to a huge turnover.

Being a Soft bookmaker is becoming very challenging nowadays, considering that the Asian market is expanding at a very quick rate. Why would I place a bet on a Soft book for a much cheaper return (and also risk being erratically limited) when I could place a much larger bet at a much better price through an Asian book?

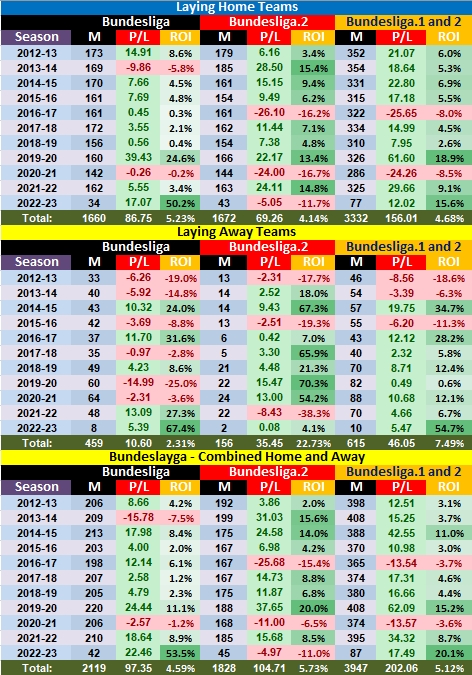

In September 2010, I noticed that the strategy of laying certain Home Favourites in the German Bundesliga was consistently profitable, making this an ideal system for mitigating Betfair's Premium Charges.

The system has been profitable in both the Bundesliga and Bundesliga.2 leagues.

Initially the system was to lay (oppose) most teams priced at odds-on but as more data has become available, the exact range has expanded.

Because this is a Laying System, it’s really only suitable to be applied on the Betting Exchanges, although you could combine backs of the Draw and away team if you were desperate.

A note on the prices used. Since I don’t have reliable historical Lay prices, I use closing price data from Pinnacle Sports, courtesy of Football-Data.co.uk, and remove the margin using the "Equal Margin" method detailed in Joseph Buchdahl's excellent book "Squares & Sharps, Suckers & Sharks".

This resulting 'fair' price is usually very close to the closing Exchange price, but remember there’s commission to pay on Exchange winning bets. In the seasons since 2012-13 for which we have the new system has lost money only once in both Bundesliga.1 (2013-14) and Bundesliga.2 (2016-17), and overall only in that one (2016-17) season.

Here’s a real life example as I write this, from Pinnacle Sports: The Lay price, calculated by removing the margin is 1.673, very close to Betfair’s 1.68.

UMPO is an acronym for Underdogs MLB Play-Off and is a simple strategy which backs odds-against underdogs in the Major League Baseball Play-offs.

Since 2004 - the first year for which I have data - it has been a steady winning strategy, and the following returns from a US site can generally be beaten on the exchanges.

Maria's Laying System achieved some notoriety in 2005-2006 when its creator (Maria Santonix) increased a starting bank of £3,000 to six figures (£100,603.78 to be precise) in 303 days.

What came to light only later was that Maria’s father was connected with several bookmakers, and through her contacts, she was able to obtain privileged information that helped with her selections. No doubt this contributed considerably to her winnings.

While most of us do not have access to the kind of data Maria had, we can still profit from her laying system. But we must state that her selections were, in fact, remarkable. Of her 4,131 selections over 303 days she achieved 3,547 wins; in other words, a strike rate of almost 86%. While Maria’s system does not in any way help us with our selections, it does provide a mathematical plan that will help us maximise our winnings.

This way of staking is actually truly excellent but it wont change a losing system into a winning one. This is something that many people need to understand before they try and replicate what Maria did. Maria felt she had a winning system for laying horses and so she used this staking plan to compound the profits and grow her bank. Something she certainly achieved by turning £3000 into £100,000 within a year!

What criteria do you use to select the lays?Ooooh, I could tell you, Atc ... but then I would have to kill you ...

The thing is that a lot more of my selections drift than shorten in the market. This is, really, how I get away with listing the selections here in the first place, to be honest, without it having much effect on the prices I lay to myself. I take loads of early laying prices if I think they'll drift, which I try to judge, with varying degrees of success by "trading-style chart-reading" on the exchange.The times that this causes me a problem are (like yesterday's accident) when it's too early to tell, for a late evening runner, because even Betfair doesn't have enough liquidity on those earlier in the day. So I just leave positions unmatched at 11.0 (just like I leave a lot of earlier ones unmatched at 7.4).I'm gradually been learning from nearly 2 years of doing this, now, that overall I make more profit and a better POI on my higher selections, and less on my lower ones. I happen to know a few full-time professional layers (mostly because my father's one of them!) and they all tell me the same thing: the way to make secure and steady income is by laying in the sort of 5.0 or 6.0 up to 15.0 bracket; nothing much shorter - with the exception of some "value shorties" which I'm stuck with for the moment anyway, because my system produces them and I'm usually pretty strict about including system selections and not just leaving them out because I "don't like the look of them" because my judgement isn't good enough to start doing that, and I'm putting it mildly!So for me, making the cut-off any shorter is an absolute no: I want to make it longer, really, not shorter. I imagine that the reality of available prices is such that if you make it 10.5 or less, you'll actually be missing out a much higher proportion of the selections than you might expect just from looking at the SP's, and really you'll end up following "selected selections" rather than "selections". It might be a good and viable and profitable system, and it might work well for you, and I'm not trying to talk you out of it at all; but it's not my system, and it's not what works for me.

It's incredibly hard work. I have, in my case, been particularly lucky to have had very good teaching (and from quite a young age!) from a very long-term successful punter who happened to be my father, an opportunity obviously not available to the overwhelming majority of punters. But it has also been very hard work, and very many years of it.

I think that a lot of people imagine that it's as easy as dreaming up a suitable system or method that works, and then just sticking to it. The reality is that that's terribly, terribly difficult to do, and things tend to have a limited shelf-life of viability and profitability anyway.

I think it's also very true that different styles and approaches suit different people.

What many people are looking for, in my opinion, is (one way or another) a "short-cut" and there really aren't any. Or at least, the ones that do very occasionally arise are pretty difficult to identify and also not so easy for many people to follow (like this thread, perhaps!). But the reality is that many people find that when they follow a successful system, it isn't successful for them, because actually following a successful system is something that some people are (for various different reasons) not so well equipped to do.

The point I'm trying to build my way up to making here is that developing, analysing, researching and using "systems" (for the benefit of those of us who are not exactly steeped in racing, barely know one end of a horse from the other and have no real, on-the-ground experience at all), isn't in any way a "quick or lazy substitute" for all

that knowledge and experience; it's every bit as time-consuming, difficult, specialised and labour-intensive as any other approach. It just entails a different sort of work.

When asked:

"is there a reasoning behind your price limits, i.e. up to 3.5, 3.6 to 7.4, 7.5 to 11?

she generously expanded on her thinking with a detailed reply:

Well, yes there was when I produced it a couple of years ago, after fiddling about with many different possibilities (and having some much more sophisticated software available then than I have now).I wanted to be able to break it up into four chunks (there's 11.5 to about 15.5 as well, but those don't appear in this thread) for all the reasons given in the thread's first couple of posts, to be able to avoid the worst features of laying either purely to fixed stakes or purely to fixed liabilities, and these turned out to be the most natural dividing lines, the first cut-off of 3.5 mostly for "money management reasons" and the second of 7.5 on "frequency" grounds (the point being that in practice, many selections that I want to lay tend to cross that line at some point during their market travels and it therefore seemed a potentially good discipline to create one's arbitrary chart/table landmark there, "waiting for 7.4" being an activity with a reasonable expectation of avoiding disappointment often enough to make it worthwhile).I haven't looked at it much since then, I'm suitably embarrassed to say, and of course there's absolutely no reason whatsoever to imagine that it would be suitable for anyone else's selections. This is why I'm always (even now) a bit taken aback when people thank me for the "brilliant staking system" which they are adopting for use with their own selections. I would actually think it far more promising if they were adapting it for use with their own selections (after studying a few thousand results in detail with appropriate spreadsheets etc. - not by "guessing"!!), rather than just adopting it! But this, I think, is really what you're asking about, and my answer is "yes; do that".

I think the overall concept of having these different price-brackets as a way of breaking the thing up, rather than using the "sliding-scale approach" of fixed liability is a valid and sound one, and constitutes a staking system which is safe and profitable if the selections are profitable at fixed liability to start with, obviously.

There will always be people who will try to come up with a staking system which will make profitable a system that wasn't profitable to start with at level stakes/liability; and even more alarmingly there will always be some who apparently manage to do it (the key word, of course, being "apparently"!), but there have to be large numbers of "new layers" coming into the markets all the time and eventually wiping themselves out: that's how markets work, I'm afraid.

The key sentence there is that the system is profitable because the selections are profitable at fixed liability, not because there is anything magical about the laying bands.

Often incorrectly written as ELO, Elo ratings actually

take their name from the inventor, Arpad Elo, a Hungarian-born American physics

professor and Chess player who invented the ratings method as a way of

comparing the skill levels of players from his game. Its use has expanded, and

has been adapted for several sports including American Football and basketball,

but also in football, and it is their use here that is the focus for the rest

of this article.

The

Basics

The essence of Elo ratings is that each team has a

rating. When comparing two teams, the team with the higher rating is considered

to be stronger. The ratings are constantly changing, and are calculated based

upon the results of matches. The winner of a match between two teams typically

gains a certain number of points in their rating while the losing team loses

the same amount. The number of points in the total pool thus remains the same.

The number of points won or lost in a contest depends on the difference in the ratings

of the teams, so a team will gain more points by beating a higher-rated team

than by beating a lower-rated team.

Raw Elo

suggests that both teams ‘risk' a certain percentage of their rating in each

contest, with the winner gaining the total pot, i.e. their rating increases by

the losing team’s ante. In the event of a draw, the pot is shared equally.

A Simple

Example

A simple example shows how this works when two evenly

matched teams meet, and both have 5% of their rating at risk. Arsenal and

Chelsea both have a rating of 1000 so both teams risk 5%, i.e. 50 points, and

the pot contains 100 points.

There are

three possible outcomes.

1) Arsenal

win, and the result of this is that Chelsea’s rating drops by 50 to 950, and

Arsenal’s rating increases by 50 to 1050.

2) Chelsea

win, and the result of this is that Arsenal’s rating drops by 50 to 950, and

Chelsea’s rating increases by 50 to 1050.

3) The result

is a draw. The pot is divided between the two teams, resulting in the ratings

for both Arsenal and Chelsea remaining unchanged at 1000.

A Second

Example

A second example shows how this works when the home side

is stronger. Manchester City (with a rating of 1200) plays Aston Villa (with a

rating of 1000). Again, both sides risk 5% (60 points and 50 points respectively),

so the pot contains 110 points.

The three

possible results and their effect of the ratings are:

1) Manchester

City win, and the result of this is that Aston Villa’s rating drops by 50 to

950, while Manchester City’s rating increases by 50 to 1250.

2) Aston Villa

win, in which case Manchester City lose their 60 points and their rating drops

to 1140, while Aston Villa gain the 60 to improve their rating to 1060.

3) The result

is a draw. The (60+50) 110 points in the pot are divided by two, resulting in

Manchester City’s rating dropping by 5 points to 1195, and Aston Villa’s rating

improving to 1005.

A Third

Example

A third example shows how this works when the away side

is stronger. Wigan Athletic (with a rating of 800) plays Manchester United

(with a rating of 1000). Again, both sides risk 5% (40 points and 50 points

respectively), so the pot contains 90 points.

The three

possible results and their effect of the ratings are:

1) Wigan win.

Their rating increases by 50 to 850, while Manchester United’s rating decreases

by 50 to 950.

2) Manchester

United win, in which case Wigan lose their 40 points and their rating drops to

760, while Manchester United gain the 40 to improve their rating to 1040.

3) The result

is a draw. The (40+50) 90points in the pot are divided by two, resulting in

Manchester United’s rating dropping by 5 points to 995, and Wigan’s rating

improving to 805.

The table

below summarises these combinations of pre-match ratings, match results, and

updated ratings:

Some

Issues

All very simple, but for football, it is much too

simple. Anyone with a basic understanding of football can see a number of

problems with the above examples. One obvious problem is that home advantage is

not taken into account, so in a match between two evenly rated teams, in the

event of a draw, the away side should be rewarded, and the home side penalised.

In the ‘teams evenly rated’ example above, a draw for Chelsea at Arsenal is

clearly a better result for them than it is for Arsenal, and it is illogical

that both teams walk away at full-time with the same rating as when the match started.

In Part Two, I will look at some ways in which these problems can

be remediated.

In Part One we explained the basic premise of Elo ratings, and illustrated how they are applied. Part two will offer some suggestions on how the principles of Elo can be enhanced to make our ratings more useful. It is important to understand that these are only suggestions. There are no hard and fast rules that dictate what these parameters should be. There is no right and no wrong, only what works and what doesn’t work.

We finished

Part One with an example of two evenly rated teams, risking the same percentage

of their ratings, and identified one major problem which is that an away draw

is better than a home draw, and it is thus illogical for both teams to end the

match with the same rating as they started.

The

Punter’s Revenge: Adjusting For Home Field Advantage

One way to handle this is by having the home team risk a

slightly higher percentage of their rating than the away team. Back in the

early 1980s, two authors, Tony Drapkin and Richard Forsyth wrote a book called “The

Punter’s Revenge: Computers In The World Of Gambling”, which was targeted at

computer literate punters at a time when the personal computer was just

becoming popular. One of the more memorable chapters was on rating football

teams, and the author’s suggestion, after running trials, was to use 7% for the

home team, and 5% for the away team. I’ve found no reason to diverge too far

from these numbers.

If we re-visit the earlier examples from part one, using the 7% and 5% numbers, the results become:

When the teams

are identically rated going in, after a drawn match, the away team gains

slightly, the home team loses slightly, something that intuitively seems right.

If you’re not happy with the adjustments that 7% and 5% give you, then there’s

absolutely no reason not to tweak these, but I would caution against exceeding

10% or going below 3%. Changes in rating should be in modest increments, but at

the same time, not too modest that it takes a season for a declining team’s

rating to reflect its form.

Result

Adjustment: Incorporating Margin Of Victory

Now to address the next problem – match results. Basic

Elo doesn’t quantify wins. A win is a win, whether it is by one goal or by a

dozen. Most readers will agree that this is an unsatisfactory state of affairs,

and will make adjustments. One method is to increase the percentages that each

team risks, but to award a certain percentage of the pool to the winners /

losers varying depending on the margin of victory / defeat.

For example,

Arsenal and Liverpool are both rated at 1000, and Arsenal are at home. The pot

(or pool) contains 120 points, 70 from Arsenal, 50 from Liverpool. If the game

finishes 6-0 to Arsenal, it’s reasonable to give all the points to them. My own

preference is for a four-goal win or more to be sufficient to secure the entire

pot. A three-goal win is pretty good, and earns most of the pool, whereas a two-goal

win earns a little less, and a one-goal win the minimum. The following table is

a suggestion.

Winning is

worth at least 70% of the pot, with the margin of victory becoming less

significant as it grows. Winning 6-0 rather than 5-0 is neither here nor there,

but winning 1-0 rather than drawing 0-0 is much more significant – even though

the difference between both pairs of scores is just one goal. You may want to

consider a 1-2 defeat as a better result than a 0-1 defeat, but again,

decisions such as these come down to personal preference. With all the time in

the world, you might analyse goal times, and conclude that a 2-0 win decided in

the 30th minute is a stronger win than a 2-0 win in which the second goal was

scored on a breakaway in the 93rd minute with the vanquished team pressing hard

for an equalizer. A fair conclusion in my opinion, and an example of how you

can modify Elo to suit your own needs, and add flexibility based on the amount

of time you have available.

Maintaining

accurate ratings is time consuming, and in previous years I would attempt to

maintain ratings for the Premier League, Football League and Conference as well

as the Scottish Leagues. These days, I restrict my tracking to the top

divisions of England, France, Germany, Italy and Spain, in part because there

is a wealth of data readily available to input, and on the output side, there

are many liquid markets available. It is also my opinion that in the lower

leagues, ratings are not so stable. A modest amount of money goes a long way,

as recently seen with Crawley Town and Fleetwood Town, and ratings can soon be

out of date.

In Part Three, I will look

at more ideas for maintaining accurate ratings.

In Part Two, I looked at one way in which Elo ratings could be improved by measuring the strength of a win based on winning margin. However, the low scoring nature of football means that the match result often does not reflect the performance of the teams.

We have all

seen games where one team has dominated, only to lose 0-1 to a goal very much

against the run of play. If you limit your input to this single figure, goals

scored minus goals conceded, you risk entering less than accurate data into

your ratings.

While it is

true that Birmingham City did beat Chelsea 1-0 on November 20th, 2010 is it

fair and reasonable to award 100% or 70% of the points available to them? You

might think it is, and I would say that is your decision to make, but my take

on it is to look behind the result and use some of the other data that is

readily available these days.

When deciding

what data I should include, my rule is that there is a correlation between the

data and goals. For example, simple logic tells you that there is a

relationship between shots, shots on target, and goals. 10 shots, of which 5

were on target, doesn’t necessarily mean that a team will score 2 goals, but

for each league there are fairly consistent ratios which we can use.

Charles

Reep: Incorporating Shots On Goal

Pioneering football statistician Charles Reep began his

research in 1950 (at 3:50pm on 18 March while watching Swindon Town play

Bristol Rovers to be precise) and discovered (among other things) "that

over a number of seasons it appears that it takes 10 shots to get 1 goal (on average)".

This average

will of course vary from season to season, by league and by team, but the

important thing is that there is a correlation between shots, shots on target,

and goals scored. A note here that some of this data has an element of

subjectivity about it, and you will often see major differences in the

statistics for the same game from individual observers.

Again, how

much effort you want to put into this is a personal choice. Researching the

leagues you are interested in will show there are differences, which you can

incorporate if you wish, for example as of 2011, the EPL is more efficient at

converting shots to goals than Serie A.

I would

however caution against changing these parameters too frequently once you have

determined reasonable values, with my preference being to use an average for

the past three seasons. The soccerbythenumbers.com website often has some

interesting articles on this subject, along the lines of this entry from

January 2011:

Adding

Meaning

This data is important because it allows you to enter

more meaningful data into your calculations. Arsenal 2 Chelsea 1 is a start,

but in my view, the data is made more valuable by entering the shots and

shots-on-target figures also, so you now have for example Arsenal 2:5:12

Chelsea 1:8:19 - a set of numbers that might reasonably lead you to conclude

that Chelsea were a little unlucky in that their goals scored were lower than

might have been expected.

You can

include other data too, although I have yet to see any evidence of correlation

between free-kicks or yellow cards. Red cards can obviously be more

significant, but you would want to factor in the amount of time remaining at

the time of the dismissal. A headline of "10 man City see of United"

might sound dramatic and sell newspapers, or draw clicks, but if the dismissal

was in the 90th minute, it's a little misleading to say the least.

In Part Four,

I'll look at corner kicks and whether this additional data should be included

in your Elo based ratings.

Dangerous

Corner

I concluded Part Three with a discussion about what data can or should be

included when adjusting a team's Elo ratings. It might seem logical and

reasonable to include corner kicks, but perhaps surprisingly, the evidence

shows that there is essentially no correlation between the number of corner

kicks and goals scored. The English Premier League is actually the strongest,

while Serie A and La Liga are the weakest.

This isn’t to say

that corners do not lead to goals. One of the problems is that the readily

available data is based on match totals, i.e. they do not reveal how many

corners lead to a goal; only that over the course of a match, Team A had 2

goals and 12 corners. Both goals may have come from corners, but at this

'macro' level, there is no evidence that says there should be say one goal for

every eight corners.

Having decided what data to include, we are no win a

position to expand upon the simple table seen in Part Two, which looked like this:

Putting

It All Together

By using more data than simply the round figure of

goals, it is possible to 'more accurately' reflect the result of a game. I

mentioned in Part Three the real-life example of Birmingham City beating

Chelsea 1-0 on November 20th, 2011, and we will use this match as an example of

how additional data can be incorporated.

Birmingham

City had one shot, and they scored one goal. Chelsea had 24 shots, 9 were on

target, yet none resulted in a goal. If we have done our analysis and concluded

that from ten shots, you can expect one goal (on average), or that from three

shots on target, one goal can be expected, you have tripled the amount of data

you are entering, and this helps to smooth out any outlying data points.

It is at this

point that a basic knowledge of spreadsheets will be useful, since the easiest

way to automate these calculations is by creating LOOKUP tables.

Using the

ratios for this example (Shots : Shots-On-Target : Goals) we have a result of

4:1:1 to 20:10:0. Dividing the first parameter by 10 (10 shots approximates to

1 goal), and the second by 3 (3 shots-on-goal approximates to 1 goal), we have

in goal units 0.4:0.33:1 to 2:3.33:0. You can average (mean or median) these

numbers out, or apply a weighting to them so that the match result becomes

Birmingham City 0.58 Chelsea1.78. Any weightings or the choice of average is a

personal preference. While Chelsea did not win the game, their overall

performance based on these numbers suggests they were the better team, and my

ratings would adjust in accord with a more accurate scale, for example:

Again, it is personal preference how granular you make these numbers. Breaking them down into 0.25 increments is one idea, but you can use any number. Once the factors are entered into your spreadsheet, and you have set the LOOKUPs correctly, they do not need to be maintained. Your spreadsheet can calculate your match result, e.g. 1.78 to 0.58 and update the Elo ratings accordingly.

Modified

Results

At this point in the process, you might also want to

consider weighting the ‘modified’ result based on the strength of the

opposition. An implied score of 1.5 to 0.5 can reasonably be considered a more

merit worthy achievement against Manchester City than against a struggling

team.

Update the Elo

ratings based on the Table A above, or your version of it, and you’re done.

Most matches will see a small change in rating for both teams, some one-sided

affairs may see a bigger shift, but the ratings, once established, ‘should’

reflect the strength of one team when compared with another.

Predictions

How do I use my ratings to make a fortune I hear you

ask? One way is to expand your spreadsheet to incorporate a predictive feature.

For predicting a future match, you would enter in the two team’s ratings, say

800 and 1000. Create a table with the same margins as there are in Table A, and

this can easily be programmed to calculate the post-match Elo ratings for each

team if the winning margin is 0, 0.25, 0.5 etc. Your spreadsheet can be coded

to display the margin of victory which will keep the ratings as close to their

pre-game position as possible. Note that you will also need to allow for the negative

equivalents to cater for away wins, and the table above would also have values

assigned for -0.25, -0.5 etc.

For example,

Wigan Athletic are currently rated at 1257, Manchester United at 1549. If Wigan

plays Manchester United at home, a margin of 0 would result in the ratings

being unchanged (top right number 0.00) as in the picture below:

If we look at

the reverse fixture between these teams using the same ratings, the spreadsheet

shows the following:

The ‘expected’

result in this example is that Manchester United will win by 1.5 goals.

If the

modified result entered is 3.21 to 0.91, (e.g. United win 3:1 and these numbers

are modified for shots and other criteria) the picture below shows how the

ratings would change. Manchester United would gain 9 points, and Wigan Athletic

would lose the same 9 points. United's win by a margin of 2.3 exceeded

expectations, so they are duly rewarded, but winning does not always boost a

team's ratings.

By entering in

all the upcoming fixtures, your spreadsheet will give you a starting point

before you bet. Whether your preference is to focus on the matches expected to

be draws, or to look for value on the Asian Handicaps based on your

computations, is up to you. I tend to focus on the draws, matches where the predicted

result is 0 to 0.5, but that’s just my preference as I consider the draw price

to be somewhat ignored, and thus be more likely to offer value.

Caution

I mentioned that this prediction is a starting point.

You should always be aware of the relevance of the match to both teams – early

and late season can be treacherous, and if you use the ratings in domestic cup

games that some teams may take less seriously than others, the spreadsheet

won’t help you.

This also

raises the question of whether you should include Cup matches in your ratings

or not. My preference is to not use domestic cup matches, but I do use

inter-league Champions League games or Europa League games to adjust my

ratings, e.g. AC Milan v Chelsea.

For anyone

interested in my starting point for these ratings, I used the 2008-09 season

standings, and used UEFAs coefficient to make the English league stronger than

the French league for example. After three years of maturity, the top four

clubs in sequence are Barcelona, Real Madrid, Manchester City and Manchester

United. The weakest is Ligue 1’s Espérance Sportive Troyes Aube Champagne –

a.k.a. Troyes.

Conclusion

This concludes the series on Elo ratings, and once

again, I would like to make it clear that many of the parameters I use area personal

preference and can be adjusted in any way you wish. The process described above

is quite possibly unique to me, as it is a combination of ideas and thoughts

collected over more years than I care to remember. It is not intended to be a

‘copy and paste’ answer for you; the purpose of these articles has been to show

you how one person’s thought process works, and perhaps prompt you to have some

ideas of your own.

There is

another component to the spreadsheet which is the use of the ‘modified result’

mentioned above as input to a Poisson calculation from which you can estimate

the probability of every result, and thus all the Over / Under, Match Odds and

Correct Score markets, and that will be the subject of a future article.

While I have tried to make this series as clear and as easy to understand as possible, it is not impossible that I have assumed some knowledge or understanding that I should not have, so if anyone has any questions on the above, please comment or send me an email, and I will try to respond.